Front desk staff are still holding on the line for twenty minutes to confirm a copay that changed three weeks ago, and billing teams are still finding out about a coverage problem only after the claim bounces back.

That’s the reality in a lot of practices right now, no matter how modern the EHR looks on the surface.

Clinics that have shifted this work to an insurance verification virtual assistant are catching those changes days before the appointment instead of weeks after the denial shows up in the aging report.

The shift isn’t really about new technology replacing old habits. It’s about who owns the check and when they run it.

Where Eligibility Gaps Turn Into Denied Claims

Here’s the part that surprises newer billers: eligibility problems rarely announce themselves early. A patient’s plan lapses, a subscriber ID changes, or a secondary payer gets added, and nobody updates the chart.

None of that shows up as a red flag at check-in. It shows up three weeks later as a denial code that everyone has to trace back to its source.

Registration and eligibility issues are the single largest driver of claim denials in the industry, accounting for nearly 27% of them, according to MGMA’s analysis of Change Healthcare’s 2020 Revenue Cycle Denials Index (MGMA, 2021).

That single category outweighs coding errors, missing documentation, and authorization problems combined in a lot of practices. And it’s almost entirely preventable if someone catches it before the claim goes out.

24 to 72 Hours Before the Visit

This is the window that matters most, and it’s also the one that gets skipped the most. A lot of practices verify insurance once, at the time a patient first schedules, and never touch it again, which works fine until a plan changes or a coverage tier resets somewhere in the weeks between.

Employer groups switch carriers mid-year without telling anyone, and a one-time check from three months ago has no way of catching that. Re-running the verification closer to the actual appointment, ideally in that 24 to 72-hour window, catches those changes before they turn into a denial.

The Day of the Appointment

By the time a patient is sitting in the waiting room, there shouldn’t be any surprises left to find. If verification happened properly in the days before, the front desk is confirming a copay, not discovering that the plan terminated two months ago. That’s the difference between a smooth check-in and an awkward conversation at the counter.

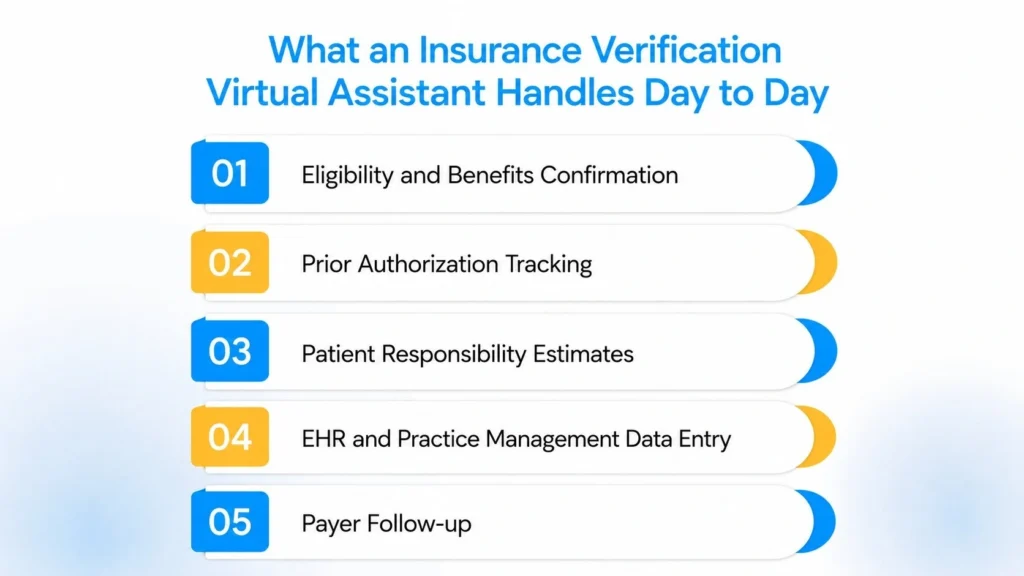

What an Insurance Verification Virtual Assistant Handles Day to Day

The job is broader than the name suggests. Most people picture someone reading benefit summaries off a screen, and that’s part of it, but not the whole picture. A verification VA typically owns:

1. Eligibility and Benefits Confirmation

This covers active coverage status, plan type, deductible and copay amounts, and whether the specific service falls under an in-network benefit. It’s the foundation on which everything else in the claim depends on.

2. Prior Authorization Tracking

Not just submitting the initial request, but watching visit counts and getting renewals filed before they lapse. Practices lose authorized visits here constantly without noticing until a denial arrives months later.

3. Patient Responsibility Estimates

Once coverage is confirmed, someone has to translate deductible and coinsurance numbers into a dollar figure that the patient can understand before they show up for the visit.

4. EHR and Practice Management Data Entry

Benefit details, authorization numbers, and coverage dates need to land in the right fields, not just in a note somewhere that nobody reads later.

5. Payer Follow-up

When a portal doesn’t have an answer or a plan requires a phone call, someone has to make that call and document what the representative said, including their reference number.

Not every practice needs all five handled by one person, since some split authorization tracking off to a specialist once volume justifies it, but the core of the role rarely changes. For a broader look at everything a virtual assistant can take on beyond verification, DoctorPapers’ guide on what virtual medical assistants actually do walks through the full scope.

Comparing Your Options for Getting Verification Done

There isn’t one right answer here, and the honest answer is that it depends on your claim volume and how complex your payer mix is.

| Approach | Best for | Trade-off |

| In-house front desk staff | Small practices with simple, stable payer mixes | Verification competes with phones, check-in, and walk-ins |

| Dedicated verification VA | Practices with rising volume or frequent plan changes | Requires a clear handoff process with your billing team |

| Fully automated eligibility software | High-volume practices with straightforward payer contracts | Struggles with ambiguous cases, coordination of benefits, and plan-specific tiers |

Software catches the easy cases fast. It’s the ambiguous ones, a patient with two active plans, a plan that shows active but has a pending termination date, where a person still needs to make a judgment call.

Whichever option you land on, compliance still has to hold up. DoctorPapers’ overview of HIPAA-compliant virtual assistants covers what to confirm before anyone, in-house or remote, gets access to patient data.

When Outsource Insurance Verification Work Makes Sense

Some practices hold onto this task internally long after it’s outgrown their front desk capacity, mostly out of habit. If your denial rate tied to eligibility issues is climbing, or your front desk is skipping re-verification because the phones don’t stop ringing, that’s usually the signal.

Practices that decide to outsource insurance verification healthcare tasks tend to do it once the calculation stops being close, not before.

The honest caveat here: whether outsourcing makes financial sense depends heavily on your specialty, your payer mix, and how much of your volume comes from plans with complicated authorization rules.

A single-specialty practice with three or four stable payers has a very different calculation than a multi-specialty group juggling forty contracts.

There isn’t a universal breakeven point, and anyone who tells you there is hasn’t looked closely at your numbers. Once you do bring someone on, the first few weeks matter more than most practices expect.

DoctorPapers’ guide on training a medical virtual assistant walks through what that onboarding period should actually look like.

Where a Medical Virtual Assistant Fits Into the Rest of Your Revenue Cycle

A well-built medical virtual assistant insurance verification workflow doesn’t operate in isolation. It’s the first domino in a chain that includes coding, claims submission, payment posting, and denial follow-up. When verification is accurate and timely, clean claims go out the door and stay clean.

When it’s rushed or skipped, the errors surface downstream, usually as a denial that costs far more time to fix than the original check would have taken.

A well-run verification workflow also changes what your billers spend their day doing. Instead of chasing eligibility problems after the fact, they’re working actual denials, appeals, and payer negotiations.

That’s a better use of a trained biller’s time, and it’s part of why practices that make this shift often see their overall denial rate drop, not just the eligibility-related slice of it.

One thing worth noting, even though it’s a bit of a tangent: patients notice this shift too. A front desk that isn’t scrambling to confirm coverage on the spot tends to run calmer visits overall, and that calm is contagious in a waiting room.

Conclusion

None of this requires ripping out your current systems or retraining your entire staff. It starts with a clear question: is verification happening consistently, on a schedule, by someone whose only job is to get it right? For a lot of practices, the answer is no, not because anyone’s careless, but because front desk staff are pulled in six directions at once.

Bringing in an insurance verification virtual assistant gives that work a dedicated owner instead of leaving it to whoever has a free minute between patients.

Practices working with DoctorPapers on their revenue cycle have found that getting this one piece right upstream tends to simplify almost everything that happens downstream.

Frequently Asked Questions

- How is this different from the eligibility check tool already built into our EHR?

The built-in tool handles the straightforward cases well: active or inactive, in-network or out. It doesn’t handle the judgment calls, though, like coordination of benefits or a plan showing active with a pending termination date sitting quietly in the background. Those situations still need a person to make a call, not just a status field to display one.

- Does a verification VA need clinical training?

No. What matters is payer terminology, benefit structures, and fluency with your specific EHR and practice management system, not a clinical background.

- How far in advance should verification happen before an appointment?

There’s no single fixed rule here, and it genuinely varies by payer and plan type. Government payers tend to stay stable close to the visit date. Some commercial plans update coverage status with almost no warning, sometimes the same week as the visit itself. A common approach is one check at scheduling and a second one 24 to 72 hours out, though a practice with heavy Medicaid managed care volume might reasonably want a tighter window than one that’s mostly commercial PPO.

- What happens if a coverage problem turns up right before the visit?

Immediately, in most cases. The VA flags the front desk and billing team right away, with the specific issue and a next step already attached rather than a vague note that something’s wrong.

- Can the same person handle prior authorization, too?

Often, yes, and it usually makes sense to keep the two together since authorization status directly affects what a claim needs before submission. Larger practices sometimes split the roles once volume gets heavy enough that one person can’t keep up with both, but that’s a scale problem more than a skills mismatch.